Starting out or switching? We’ll help you find the best card machine for your business – and we’ll get you onboard with us quickly, with all the customer service and tech support you need. We fund you fast to keep that cashflow moving.

Ways to pay

All-in-one merchant services

We’re a one-stop-shop to help you grow your business: from flexible finance options to all the services and technology you need to take fast, safe payments.

Help to run your business

We can help you work smarter and keep ahead of customer expectations, with expert advice and POS software that helps you manage your business.

Fast funding

Cashflow is critical to cover everyday operations but also those unexpected expenses. We help drive cashflow into small businesses with next-day funding into your account.

Secure payment systems for small business

Card machines

At your counter or on the go, we've got card machines for small businesses to take safe, convenient payments.

Online payments

Trade online with a safe payments gateway that protects your customers' data – and your reputation.

On the phone

Take payments over the phone without compromising on security. We’ve got a choice of systems for you.

All ways to pay

Want more than one payment method? We’ll tailor-make your package to let customers pay how they like.

“Elavon gives me the opportunity to look after my business properly – and if there are any problems, customer service solves them quickly. With Elavon, it’s really easy.”

Mohammed Mrabat, owner of Mo’s Pizza and Café Diem

For every small business, in every sector

Cafés, bars and restaurants

If you’re a café, bar or restaurant owner, your payment system needs to fit with your business’ size and sector. We’ll build your system to meet your needs. Whether customers pay at the bar, till or at the table, we’ll make it fast, safe and simple.

Hotels and guesthouses

From check-in to check-out, from room service to bar service, payments in the hospitality business seem to happen everywhere at once. We’ll help you deliver speedy service and easy, reliable transactions to help guests feel at home.

Online and in-store retailers

If you want a hosted payments gateway or a fully integrated API, or even if you want to build a multifunctional ecommerce website, our payments systems for online businesses are simple, secure and convenient.

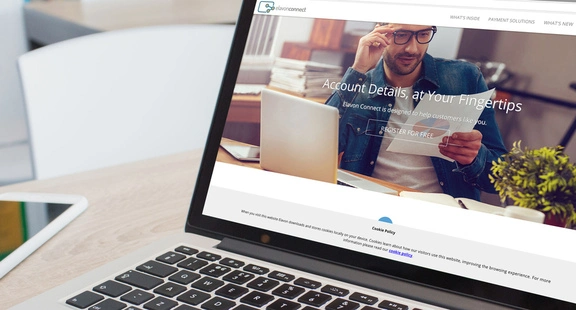

Elavon Connect – account details at your fingertips

Log into our online portal Elavon Connect for statements, account management tools, product alerts and more. With instant access to all your processing activity, you can track transactions, spot trends and growth opportunities, and help you plan your business better. Elavon Connect is a small business’ best friend.

More from businesses like yours

Monkton Elm: an omnichannel retailer

Hear how an award-winning destination garden centre is meeting changes in buyer behaviour and customer expectations by taking its business online with Elavon.

Mo’s Pizza: a hospitality customer

Expanding a daytime coffee shop into a pizza restaurant by night was easy with Poynt and Elavon Connect, leaving Mo to focus on the food and his customers.

McMullans: a retail boutique customer

Hear how Elavon helps this century-old fashion retailer to stay bang on trend with payments technology and expand its customer base so it doesn't need to rely on footfall.

Why choose Elavon?

-

Rest easy; we have your back. Just call us or tap into our online tools whenever you need help. Useful data and real-time reports tell you a thing or two about how – and where – your business is going.

Rest easy; we have your back. Just call us or tap into our online tools whenever you need help. Useful data and real-time reports tell you a thing or two about how – and where – your business is going.

-

Blink and the world looks different. That’s okay: our plans and solutions flex as your business changes. Choose off-the-shelf simplicity or customised, multichannel solutions, built together with our awesome partner network.

Blink and the world looks different. That’s okay: our plans and solutions flex as your business changes. Choose off-the-shelf simplicity or customised, multichannel solutions, built together with our awesome partner network.

-

The right payment types, everywhere you do business. Stepping into new markets together, we’ll arm you with the right tools and support to meet your customers’ needs, wherever they are and however they want to pay.

The right payment types, everywhere you do business. Stepping into new markets together, we’ll arm you with the right tools and support to meet your customers’ needs, wherever they are and however they want to pay.

“Our electronic point-of-sale system controls our inventory all the way through to the receipt of the funds at the end of the processing period, with the reliability of knowing we're going to receive the cash in our account the following day.”

David Bellman, head of finance, Monkton Elm Garden Centre

FAQs

Need a card reader for small business? To accept debit and credit card payments in a retail location – like a café or store – you need a merchant account and point-of-sale (POS) system with a card reader or a card machine.

What card payment machine you need should depend on where your want to serve your customers. When it comes to card machines for small businesses, that could be at the counter, on the move, over the phone or over your website. You should also consider what cards you want to accept.

Countertop debit and credit card machines stay in one place, so they're perfect for shops and stores. A wireless card terminal is handy for businesses where you need to move around, like restaurants. You can accept cards anywhere, using your mobile phone, through mobile payment processing apps like Elavon Mobile: this is 'pay as you go' and also great for on-the-go sales.

Modern systems, such as Elavon electronic points of sale (EPOS), include hardware and software that let you process both card and cash transactions.

Any business that wants to sell online will need a payment gateway as well as a merchant account. Virtual terminals are through a computer and are great for businesses taking orders over the phone or online. You don't even need a website – Virtual Terminal lets you generate a secure, specific payment URL, which you can then email or text to the customer to make the payment.

A merchant account is a type of bank account that allows you to accept electronic transactions such as debit and credit card payments. All businesses that want to accept electronic payments need a merchant account.

Be sure your card machine takes all kinds of cards like credit and debit. It should also work with contactless payments like Apple Pay and Google Pay. Some of the major card networks that businesses should accept include: Visa, Mastercard, Discover, JCB and American Express.

The best card reader for small business will offer a versatile and affordable way to take payments from customers. Whether you run a retail store, a restaurant, pop-up shop or any other type of small business, you’ll need a way to take card payments.

Mobile devices take all major payment types and offer reliable connectivity, so you have the flexibility to trade wherever your customers are. Other things to consider include faster payment options, security of payments and where your customers are.

Fees incurred for processing card payments can be roughly split into two types: fees incurred for each specific transaction and monthly or one-off costs charged for the payment services and hardware.

Compliance with the Payment Card Industry Data Security Standard (PCI DSS) can help companies protect cardholder payment account data. PCI DSS compliance is an industry mandate. For that reason, you should consider PCI compliance one of your critical payment system features. The easiest course of action is to find a partner that handles this for you.

There are four levels of business classification that the PCI assigns based on the number of transactions a business makes.

Level 4: Fewer than 20,000 card transactions per year

Level 3: Between 20,000 to 1 million card transactions per year

Level 2: Between 1-6 million card transactions per year

Level 1: More than 6 million card transactions per year

When someone pays by card, a request gets sent to their card issuer by the payment processor to check the transaction and authorise it. They send a code back to the till so the payment can go through. It all costs money for the payment processor, and that gets passed on to you, the merchant, as a fee. You might see it shortened to ‘auth fees’.

A card scheme or card brand are those companies that provide the payment networks allowing for card payments. The most common are Visa and Mastercard, but you’ll also see American Express, Discover, JCB and China UnionPay. They also set the rules to keep the system running and safe.

Card issuers are the organisations that gives (or issues) debit or credit cards to cardholders. It’s often, but not always, a bank which manages the account. An example would be your current account debit card. Most card issuers are not card schemes, but some card schemes work as card issuers as well.

Not to be confused with a refund. If someone questions a payment on their card statement and then claims the money bank through the card-issuing bank or credit card company, that’s known as raising a ‘chargeback’. It’s often because they suspect fraud which will then trigger an investigation into whether it really was fraudulent and, if so, who should pay back the money as well as any fines. A refund is between you and your customer but, because it leaves you out of pocket, the two terms are often mixed up.

A 'batch' is the way lots of different payments get grouped together to make it easier to process and settle those payments. So, a restaurant might combine all the payments they take each day and submit the combined batch to us rather than sending us each individual payment.

Get in touch

Click below to contact an Elavon payments expert.

Helping thousands of customers around the world grow their business through payments

Customer service and support

We’re here to help!

Customer service: 0818 20 21 20

Telephone: Monday to Friday, 8am to 5pm

Chat: Monday to Friday, 8am to 6pm

Elavon technical support: 0818 30 31 30

24 hours a day, 365 days a year

Opayo product support: 01 240 8731

24 hours a day, 365 days a year

Privacy policy

Data Privacy Notice

Cookie policy

Accessibility statement

Legal

Modern slavery act

Our Regulatory Status

Copyright© 2025 | U.S. Bank Europe DAC. Registered in Ireland – Number 418442. Registered Office: Block F1, Cherrywood Business Park, Dublin 18, D18 W2X7, Ireland.

U.S. Bank Europe DAC, trading as Elavon Merchant Services, is regulated by the Central Bank of Ireland.

We are regulated by the Central Bank of Ireland for our acquiring, transaction risk analysis, and dynamic currency conversion services. For all other products and services we provide, please note the following: Warning: The provision of this service does not require licensing, registration, or authorisation by the Central Bank of Ireland, and as a result is not covered by Central Bank of Ireland rules designed to protect consumers or by a statutory compensation scheme.

Helping thousands of customers around the world grow their business through payments

Customer service and support

We’re here to help!

Customer service: 0818 20 21 20

Telephone: Monday to Friday, 8am to 5pm

Chat: Monday to Friday, 8am to 6pm

Elavon technical support: 0818 30 31 30

24 hours a day, 365 days a year

Opayo product support: 01 240 8731

24 hours a day, 365 days a year

Privacy policy

Data Privacy Notice

Cookie policy

Accessibility statement

Legal

Modern slavery act

Our Regulatory Status

Copyright© 2025 | U.S. Bank Europe DAC. Registered in Ireland – Number 418442. Registered Office: Block F1, Cherrywood Business Park, Dublin 18, D18 W2X7, Ireland.

U.S. Bank Europe DAC, trading as Elavon Merchant Services, is regulated by the Central Bank of Ireland.

We are regulated by the Central Bank of Ireland for our acquiring, transaction risk analysis, and dynamic currency conversion services. For all other products and services we provide, please note the following: Warning: The provision of this service does not require licensing, registration, or authorisation by the Central Bank of Ireland, and as a result is not covered by Central Bank of Ireland rules designed to protect consumers or by a statutory compensation scheme.

Essential cookies enable core functionality such as page navigation and access to secure areas. The website cannot function properly without these cookies; they can only be disabled by changing your browser preferences. Please see our Cookie Policy for further information.

Performance cookies help us to improve our website by collecting and reporting information on its usage (for example, which of our pages are most frequently visited).

These cookies and similar technologies gather information about your browsing habits. They remember that you've visited a website and share this information with other organisations, such as advertisers and platforms on which we advertise. They do this in order to provide you with advertisements that are more relevant to you and your interests. These cookies and similar technologies gather information about your browsing habits. They remember that you've visited a website and share this information with other organisations, such as advertisers and platforms on which we advertise. They do this in order to provide you with ads that are more relevant to you and your interests.

These cookies are stored under a different domain than www.elavon.ie. They are mostly used to track you between websites and display more relevant advertisements between websites.

Find out more about cookies on https://www.allaboutcookies.org